.png?width=500&height=500&name=PSYMPL_ICON+SET-04%20(1).png)

Table of contents

.svg)

Customer experience in financial services has evolved from a nice-to-have feature into the primary battleground where banks, credit unions, and investment firms compete for market share. Modern financial institutions must deliver seamless, personalized experiences across every touchpoint to retain customers and drive growth in an increasingly competitive landscape. The days when customers would tolerate long wait times, complex processes, and impersonal service are over.

Technology giants like Amazon and Apple have fundamentally changed what consumers expect from all service providers, including their financial institutions. Customers now demand the same level of convenience, speed, and personalization from their bank or financial advisory firm that they receive from their favorite retail apps. This shift has forced financial services companies to rethink their entire customer experience strategy.

The stakes have never been higher for getting customer experience right. Institutions that fail to meet evolving expectations face declining customer loyalty, reduced profitability, and potential obsolescence as fintech startups and digital-first competitors capture market share. Understanding how to leverage emerging technologies while addressing the unique challenges of financial services will determine which organizations thrive in the coming years.

Why Customer Experience Matters More Than Ever In Finance

Financial institutions now face heightened customer expectations for personalized, seamless interactions across all touchpoints. Banks that excel in customer experience achieve 1.9x higher recommendation rates and 2.1x higher cross-selling likelihood, while poor experiences drive customers to competitors who better understand their needs.

Defining Customer Experience In Financial Services

Customer experience in financial services encompasses every interaction a customer has with their financial institution across all channels and touchpoints. This includes digital platforms, branch visits, phone support, and automated systems. A consistent, personalized experience across these touchpoints is imperative for reinforcing the institution’s brand.

The experience extends beyond basic transactions to include how well institutions understand customer needs and deliver personalized solutions. Modern customers expect fluid, personalized interactions whether they use mobile apps, ATMs, websites, or call centers.

Key components include:

- Response time and resolution efficiency

- Consistency across all channels

- Personalization based on customer data, including financial psychographic insights

- Ease of use for complex financial tasks

Financial services customer experience differs from other industries due to the sensitive nature of financial data and regulatory requirements. Trust becomes paramount when customers share personal financial information.

The experience must balance security measures with convenience, ensuring customers feel protected without creating friction in their interactions.

Impact Of Customer Experience On Retention, Loyalty, And Acquisition

Poor customer experience directly impacts financial institutions' ability to retain existing customers and attract new ones. Research shows that 88% of customers consider experience as important as the product itself.

An example to illustrate this point involves a major car company that did a study on its U.S.-based customers to determine what had the greatest impact on satisfaction and loyalty. They segmented the customer audience into two groups:

- Customers who purchased a car that worked perfectly and needed no maintenance;

- Customers who purchased a car that needed service or repairs

Thus, customer retention rates improve significantly when institutions deliver superior experiences. Customers who encounter friction during interactions are more likely to switch providers, especially in competitive markets with multiple options.

Acquisition benefits include:

- Higher conversion rates from prospects

- Positive word-of-mouth referrals

- Reduced marketing costs per new customer

- Stronger competitive differentiation

Loyalty manifests through increased engagement with the institution's services. Satisfied customers explore additional products and maintain longer relationships with their primary financial provider.

Customer experience has evolved from a supporting function into a strategic imperative that directly impacts business growth. Institutions that prioritize experience see measurable improvements in customer lifetime value.

Positive Customer Experience And Its Effect On Trust And Wallet Share

Trust forms the foundation of all financial relationships, making customer experience critical for building and maintaining confidence. Customers must feel secure when sharing sensitive financial information and making important monetary decisions.

Positive experiences build trust through consistent, reliable service delivery. When customers receive accurate information and efficient problem resolution, they develop confidence in their institution's capabilities.

Trust indicators include:

- Transparent communication about fees and policies

- Proactive fraud protection measures

- Quick resolution of issues or disputes

- Consistent service quality across channels

Wallet share represents the percentage of a customer's total financial business an institution captures. Banks that deliver excellent customer experiences achieve up to 16.5% growth in deposit share.

Customers consolidate their financial relationships with institutions they trust. This includes checking accounts, savings, loans, investments, and insurance products.

Higher wallet share reduces customer acquisition costs while increasing revenue per customer. Trusted institutions become the primary financial partner for major life events and decisions.

How Customer Expectations Are Shaped By Other Industries

Financial services customers no longer compare banks solely to other banks—they measure every interaction against the seamless experiences delivered by Amazon, Netflix, and Uber. This cross-industry benchmarking has fundamentally altered what customers expect from their financial providers in terms of speed, personalization, and digital sophistication.

Comparison Of Financial Services With Leading Consumer Experiences

Netflix's recommendation engine sets the standard for personalized content delivery that financial institutions must match. Customers expect their banking apps to anticipate needs and suggest relevant products with the same precision that streaming services recommend movies.

Amazon's one-click purchasing has conditioned users to expect instant transactions. Traditional wire transfers that take 3-5 business days feel antiquated when customers can order products and receive them the same day.

Key Experience Benchmarks:

- Netflix: Personalized recommendations based on behavior patterns

- Amazon: One-click transactions and same-day fulfillment

- Uber: Real-time tracking and transparent pricing

- Apple: Intuitive interface design and seamless device integration

Uber's real-time tracking creates expectations for transparency in financial processes. Customers want to see loan application progress and investment performance with the same visibility they have for ride-sharing services.

Apple's ecosystem integration influences how customers expect their financial accounts to work across devices. Seamless transitions between mobile, desktop, and tablet interfaces are no longer optional features—they are baseline requirements.

Expectations For Personalization, Speed, And Consistency

Modern consumers expect immediate responses across all touchpoints after experiencing instant gratification from consumer apps. Digital banking platforms must prioritize mobile-first strategies to meet these speed expectations.

Personalization has evolved beyond using a customer's name in emails. Spotify's Daily Mix playlists demonstrate the level of behavioral analysis customers now expect from their financial providers.

Banks must deliver consistent experiences whether customers interact through mobile apps, websites, or physical branches. Discord's seamless cross-platform messaging sets the benchmark for omnichannel consistency.

Speed Expectations by Transaction Type:

- Account balance inquiries: Instant

- Fund transfers: Under 30 seconds

- Loan pre-approval: Same day

- Customer service response: Under 2 minutes

Machine learning algorithms from e-commerce platforms have trained customers to expect predictive financial advice. They want their bank to suggest budget adjustments before overspending, similar to how Google Maps suggests alternate routes before traffic builds.

Wealth Management Clients And Digital-First Personalization

High-net-worth individuals increasingly expect the same digital sophistication they receive from luxury brands like Tesla and Rolex. AI-driven personalization in wealth management must match the customization levels found in premium consumer experiences.

Luxury e-commerce sites provide detailed product histories and provenance information. Wealth management clients expect similar transparency about investment origins, performance history, and risk factors.

Private banking clients compare their advisor interactions to concierge services from premium hospitality brands. The Four Seasons' anticipatory service model influences expectations for proactive portfolio management and market insights.

Digital Features Wealthy Clients May Expect:

- Real-time portfolio performance dashboards

- Predictive market analysis alerts

- Customizable risk assessment tools

- Virtual reality investment property tours

Rolex's craftsmanship storytelling approach shapes how many clients want to understand complex financial products. They expect detailed explanations of investment strategies presented with the same attention to detail that luxury brands use for product narratives. However, other clients may just want a topline of results without granular details, which may frustrate them or test their patience. This is why it’s important to understand the psychographic profile of each client, to address their personality, attitudes, and motivations.

Tesla's over-the-air updates create expectations for continuously improving financial platforms. Wealth management clients expect their tools to enhance functionality automatically without requiring manual updates or new downloads.

The Cost Of Falling Behind In Customer Experience

Financial institutions face significant consequences when they fail to prioritize customer experience, including substantial customer loss and reduced market share. The financial impact extends beyond immediate revenue loss to long-term competitive disadvantage against digital-first competitors.

Risks Of Neglecting Customer Experience

Banks that neglect customer experience face severe retention challenges, with customer retention rates dropping as much as 20% after failing to adopt adequate technological innovations. This represents a direct threat to the institution's customer base and revenue stability.

Traditional banks and financial advisory firms have already lost market share to experience-focused fintechs that prioritize seamless digital experiences. These challengers attract customers by offering intuitive interfaces and streamlined processes that established banks struggle to match.

The competitive landscape has shifted dramatically. Digital natives now represent a growing proportion of business banking customers, making superior customer experience a requirement rather than an advantage.

Key financial risks include:

- Direct revenue loss from customer defection

- Increased customer acquisition costs to replace lost clients

- Reduced cross-selling opportunities

- Weakened brand reputation in competitive markets

Examples Of Poor Customer Experience Leading To Provider Switching

Customers abandon financial providers when basic digital services fail to meet expectations. Complex account opening processes, slow transaction processing, and poor mobile app functionality drive customers toward competitors with smoother digital experiences.

Business customers particularly value integrated solutions that connect with their existing accounting and payment systems. Financial institutions that fail to provide these integrations lose clients to fintech companies offering comprehensive business management tools.

Poor customer service interactions create lasting negative impressions. When clients encounter difficulties resolving issues through traditional channels, they seek providers with more responsive support systems.

Common switching triggers:

- Lengthy approval processes for loans or credit

- Inadequate mobile banking functionality

- Limited integration with business software

- Unresponsive customer support channels

- Lack of real-time transaction visibility

Importance Of Consistent, Personalized Experience To Prevent Churn

Consistent experiences across all touchpoints build customer confidence and reduce switching likelihood. Customers expect seamless transitions between mobile apps, websites, and physical branches without losing functionality or requiring repeated authentication.

Personalized services demonstrate value to individual customers. Financial institutions that leverage customer data to offer relevant products and tailored advice create stronger relationships that resist competitive pressure.

Trust forms the foundation of financial relationships. When customers receive consistent, personalized attention similar to how a barista builds familiarity with regular customers, they develop loyalty that extends beyond simple product features.

Essential personalization elements:

- Customized product recommendations based on usage patterns

- Proactive financial guidance and alerts

- Flexible service options matching customer preferences

- Recognition of customer history across all interactions

The Role Of Technology In Shaping Modern Customer Experience

Technology fundamentally transforms how financial institutions deliver personalized services through artificial intelligence and predictive analytics. Modern systems enable real-time customer insights while maintaining consistency across digital and physical touchpoints through comprehensive data analysis beyond traditional demographic markers.

AI, Automation, And Data Insights In Customer Experience

Artificial intelligence enables financial institutions to analyze customer behavior patterns in real-time. AI-driven personalization has become essential as 72% of customers consider it crucial in financial services.

Machine learning algorithms process transaction histories to predict customer needs. Banks can identify when customers might need loan products or investment advice before they explicitly request these services. This proactive approach reduces wait times and increases satisfaction.

Automated systems handle routine inquiries while complex issues route to human agents. Chatbots resolve account balance questions and transaction disputes within seconds. The technology learns from each interaction to improve future responses.

Key AI Applications:

- Fraud detection and prevention

- Credit risk assessment

- Investment recommendations

- Automated customer support

- Predictive maintenance for accounts

Data analytics platforms consolidate information from multiple touchpoints. Customer service representatives access complete interaction histories during calls. This eliminates the need for customers to repeat information across different departments.

Personalization At Scale And Omnichannel Consistency

Technology enables seamless experiences across multiple channels from mobile apps to physical branches. Customers start mortgage applications on smartphones and complete them on desktop computers without losing progress.

Cloud-based systems synchronize customer data across all platforms instantly. Account updates made through mobile apps appear immediately in online banking portals. Branch staff access the same real-time information during in-person visits.

Personalization engines customize product recommendations based on individual financial goals. Young professionals see investment options while families receive mortgage refinancing offers. The system adapts messaging tone and product complexity to match customer sophistication levels.

Omnichannel Integration Features:

- Single customer view across platforms

- Consistent branding and messaging

- Real-time data synchronization

- Cross-channel conversation continuity

Financial institutions use API integrations to maintain service quality standards. Whether customers interact through voice assistants or video calls, they receive identical information and service levels.

Psychographic Data Beyond Demographics And Transactions

Advanced analytics examine customer behavior patterns beyond age and income brackets. Financial institutions analyze spending habits, risk tolerance, and communication preferences to create detailed customer profiles.

Behavioral data reveals when customers respond to digital versus human interactions. Some clients want complex investment discussions with advisors while others prefer self-service options for routine transactions. Some clients have a higher appetite for risk while others are more risk averse and prioritize loss avoidance. These are psychographic characteristics that comprise a client’s “financial personality.” Psychographics pertain to people’s attitudes, values, personalities and lifestyles, and are core to their motivations, priorities, and communication preferences. Systems route inquiries based on these preferences automatically.

Psychographic Indicators:

- Risk appetite - Conservative vs aggressive investment preferences

- Communication style - Formal vs casual interaction preferences

- Decision-making speed - Quick vs deliberative choice patterns

- Technology adoption - Digital-first vs traditional channel usage

Because of the differences among psychographic segments, there are optimal engagement strategies for each, from the wording of a message to the channel and frequency of delivery. Psychographic AI can be employed to generate segment-specific content that resonates with each client’s psychographic profile and motivations, resulting in more persuasive and satisfying experiences.

Social media sentiment analysis provides insights into customer satisfaction levels. Banks monitor public comments about their services to identify potential issues before they escalate. This data supplements traditional surveys and feedback forms.

Lifestyle data helps institutions time product offers appropriately. Recent home buyers receive insurance quotes while graduate students see education loan refinancing options. The timing aligns with major life events when financial needs change.

How Financial Institutions Can Elevate Customer Experience

Financial institutions can transform customer experience through strategic mapping of customer journeys, unified data integration, AI-powered personalization, consistent advisor training, and specialized technology platforms. These approaches address the core challenge that digital transformation hasn't necessarily improved customer experience despite technological advances.

Mapping And Understanding Customer Journeys

Customer journey mapping reveals pain points and opportunities across every touchpoint in the financial services experience. Financial institutions must document each interaction from initial awareness through account opening, ongoing service, and potential account closure.

The mapping process begins with identifying key customer segments and their unique pathways. Retail banking customers follow different journeys than commercial clients or wealth management customers.

Critical touchpoints include:

- Initial research and comparison shopping

- Application and onboarding processes

- Day-to-day transaction management

- Problem resolution and support interactions

- Product expansion and cross-selling moments

- Cultivation of “brand ambassadors” and chatleader influencers among clients

Journey maps should capture emotional states and psychographic preferences at each stage. Customers often experience frustration during account opening or anxiety when resolving financial issues. Understanding these emotions helps institutions design more empathetic responses.

Data collection from multiple channels provides the foundation for accurate journey mapping. This includes website analytics, mobile app usage, call center interactions, and branch visits.

Breaking Down Data Silos For Unified Customer Views

Data orchestration strategies help financial institutions integrate customer insights across departments and systems. Most financial institutions store customer information in separate databases for checking accounts, credit cards, loans, and investment products.

Unified customer profiles combine transactional data, interaction history, preferences, and behavioral patterns. This 360-degree view enables personalized service regardless of the channel customers choose.

Key integration points include:

- Core banking systems

- Customer relationship management platforms

- Marketing automation tools

- Contact center software

- Mobile and web applications

Real-time data synchronization ensures consistent information across all touchpoints. When customers call after visiting a branch, representatives can access complete interaction history immediately.

Privacy and security protocols must govern data integration efforts. Financial institutions need robust consent management and data governance frameworks to protect customer information while enabling personalization.

Leveraging AI For Personalization And Intent Recognition

Artificial intelligence transforms raw customer data into actionable insights for personalization. Machine learning algorithms identify patterns in customer behavior to predict needs and preferences.

Intent recognition technology analyzes customer communications to understand underlying goals. When customers contact support, AI can determine whether they want to dispute a charge, apply for credit, or close an account.

Psychographic AI can generate hyper-personalized content specific to each customer’s psychographic profile to resonate with their motivations and personal goals, enhancing the likelihood of persuasion and satisfaction.

AI applications in financial services include:

- Chatbots for routine inquiries and transactions

- Recommendation engines for relevant products

- Fraud detection and prevention systems

- Predictive analytics for customer lifecycle management

- Natural language processing for sentiment analysis

- Marketing and educational content generation

Personalization engines deliver customized content, product recommendations, and service options. These systems consider factors like account history, life stage, financial goals, psychographic profiles, and communication preferences.

AI-powered tools also optimize staff productivity by routing complex inquiries to appropriate specialists,providing real-time guidance during customer interactions, and content generation that activates desired customer behaviors..

Training Advisors For Consistency Across Channels

Strategic customer experience requires omnichannel consistency that maintains quality standards whether customers interact through branches, phone, chat, or digital channels. Staff training programs must emphasize uniform service delivery, hyper-personalization, and brand representation.

Comprehensive training covers product and customer knowledge, communication skills, and technology proficiency. Advisors need deep understanding of all available products and services to provide accurate guidance and a deep understanding of customer psychographic profiles to anticipate their needs and effectively position solutions in a way that resonates with them.

Training components include:

- Customer service protocols and scripts

- Conflict resolution and de-escalation techniques

- Regulatory compliance requirements

- Technology platform navigation

- Cross-selling and upselling best practices

- Customer insights (including psychographics) to enhance engagement

Role-playing exercises prepare advisors for challenging scenarios like loan rejections, fee disputes, or account closures. Regular assessment and feedback sessions maintain service quality standards.

Ongoing education keeps advisors current with new products, policy changes, and market conditions. Financial institutions should provide continuous learning opportunities rather than one-time training events.

Psympl As An Enabler Of Customer Experience Strategies

Psympl provides financial institutions with specialized tools for implementing customer experience improvements. The platform integrates customer data from multiple sources to create comprehensive psychographic profiles and create the content that resonates with these “financial personalities.”

Platform features support:

- Real-time customer psychographic segment classification

- Automated workflow triggers

- Performance dashboards and metrics

- Integration with existing technology stacks

- Compliance reporting and audit trails

The platform's machine learning algorithms continuously refine personalization strategies based on customer responses and outcomes. This adaptive approach improves recommendation accuracy over time.

Implementation typically involves data integration, staff training, and gradual rollout across customer segments. Psympl's support team provides guidance throughout the deployment process to ensure successful adoption.

Making CX Your Competitive Advantage

Customer experience in financial services has become a primary differentiator in today's competitive landscape. Financial institutions that prioritize CX strategies see measurable improvements in customer satisfaction and retention rates.

The implementation of AI, personalization, and omnichannel approaches transforms how customers interact with their financial providers. These technologies enable institutions to deliver seamless experiences across all touchpoints.

Key benefits include:

- Increased customer loyalty and trust

- Reduced operational costs through automation

- Enhanced regulatory compliance

- Improved competitive positioning

Modern financial services firms compete primarily on customer experience, making CX investments essential for long-term success. Organizations that fail to adapt risk losing customers to more agile competitors.

Ready to transform your customer experience strategy?

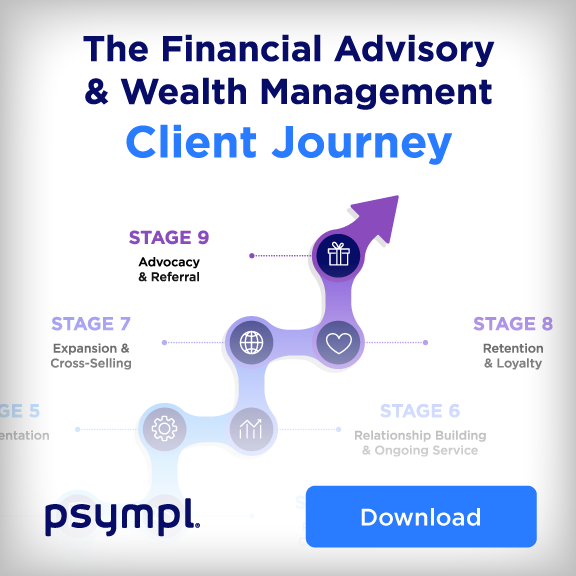

To help you see where your organization stands, we’ve created Psympl’s Buyer Journey CX Infographic — a visual guide to understanding each stage of the financial customer journey and how personalization can transform the experience.

Brent Walker

Table of contents